Balancing business growth and revenue mobilisation in new budget

The government’s immediate priority must now be strict market monitoring to ensure that these cost-saving benefits are actually passed on to everyday consumers.

The newly proposed budget initiatives aimed at curbing inflation, reducing the cost of doing business, and improving the overall investment climate is a welcome move. However, the expanding list of tax exemptions risks driving up tax expenditures at a time when the budget offers few significant measures to substantially boost revenue collection in the upcoming fiscal year.

The proposals to lower the cost of doing business are highly commendable. These include reducing Tax Deducted at Source (TDS) and Value Added Tax Deducted at Source (VDS) rates, lowering customs duties, reducing the financial cost of filing appeals with Tax and VAT appellate forums, and rationalizing business expense disallowance provisions. The government's immediate priority must now be strict market monitoring to ensure that these cost-saving benefits are actually passed on to everyday consumers.

To further boost competitiveness, corporate tax rates for unlisted companies should have been aligned more closely (20-25%) with competing regional economies. In particular, a lower rate would benefit manufacturers and equity-driven companies that generate high employment. Similarly, the turnover tax rate (1%) should have been reduced to alleviate the real financial burden on smaller businesses in the current economic climate.

Keep updated, follow The Business Standard's Google news channel

Keep updated, follow The Business Standard's Google news channel

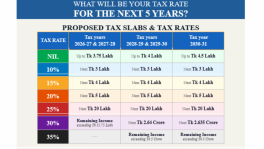

On the personal income tax front, tax slabs should have incorporated Consumer Price Index (CPI) indexation so inflation does not unfairly penalize taxpayers. Furthermore, the top marginal tax rate requires a cautious re-evaluation, given that the effective tax rate can climb to around 44%. It is also worth noting that beyond the welcome measures targeting business costs, the budget lacks structural reforms regarding VAT and customs tariff frameworks.

Nevertheless, the duty rationalisation aimed at fostering industrialisation and employment generation is a praiseworthy step. Moving forward, to expand the tax net effectively, the National Board of Revenue (NBR) must ensure compliance monitoring is smooth and transparent, protecting taxpayers from harassment while securing due revenue for the exchequer. To broaden the tax base permanently, we must ensure that all financial transactions of VAT- and tax-registered entities are fully and accurately reflected in their returns.

Finally, we must periodically audit tax exemptions to verify that they are achieving their intended economic goals, benefiting consumers, and preparing our local industries for imminent LDC graduation. While the proposed deregulation initiatives to ease doing business are excellent, the government must execute a time-bound implementation plan before the new fiscal year begins to ensure these reforms translate into less bureaucracy and a better business environment on the ground.

Failure to expand the tax net and tax base inevitably increases the burden on existing taxpayers. Chanakya famously warned that just as one does not pluck unripe fruit, a ruler should not prematurely exhaust the wealth of citizens—doing so only fuels public anger and destroys the future revenue base. Let us all come forward and contribute our part toward the country's development.

Snehasish Barua is the managing director of Smac Advisory Ltd.